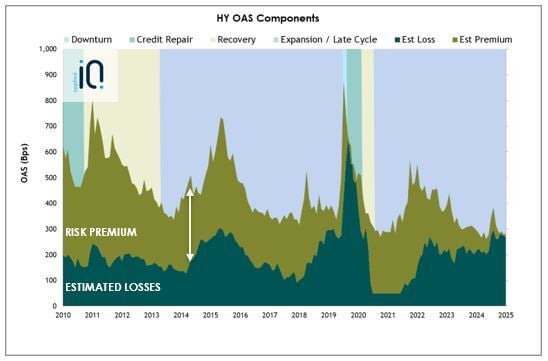

When it comes to assessing value across various fixed income credit markets, we believe the big picture is essential. For the Full Discretion team, the big picture means analyzing where we are in the credit cycle and calculating the current risk premium, defined as a market’s option-adjusted spread (OAS) less our estimated one-year-forward losses from downgrades and defaults.

We believe risk premiums can help determine the likelihood of positive excess returns more effectively than spreads alone. We often observe credit cycle stages where spreads are tight relative to history, and it’s less clear how much risk should be taken. On the other hand, when spreads are wide, many think it’s a good time to pile into higher yielding securities because they don’t consider the potential for escalating losses. Instead of only taking a narrow view of spreads, our risk premium framework focuses on expectations for losses due to default and downgrade. Risk premium is simply the gap between spreads and estimated losses.

The risk premium only moves because of a change to spreads or our estimated loss expectations, which typically results in less volatility. Downgrades and defaults are often cyclical and tend to be less turbulent than spreads, providing potential opportunities for the Full Discretion team to better identify relative value in credit markets. The combination of where we are in the credit cycle and how much risk premium is available provides three unique insights.

Risk premium:

- gives us an unemotional measure of value in the market

- guides how much risk our products should be taking

- helps us compare opportunities as we allocate across asset classes as well as the public and private options within each

Estimated High Yield Risk Premium Components Over Time

Source: Loomis Sayles, Bloomberg and Moody’s, as of 9/30/2025. OAS is based on the Bloomberg US Corporate High Yield Index.

The chart presented is shown for illustrative purposes only. Some, or all, of the information on these charts may be dated, and, therefore, should not be the basis to purchase or sell any securities. The information is not intended to represent any actual portfolio managed by Loomis Sayles.

This analysis is based on historical data and does not predict future results. Therefore, the use of this type of information to make investment decisions has inherent limitations. Markets may behave very differently than history suggests, it is not possible for any methodology to accurately identify and interpret all relevant market events.

Any investment that has the possibility for profits also has the possibility of losses, including the loss of principal.

Please see the Risk Premium Disclosure Statement for additional important information.

Past performance is no guarantee of future results.

The CHIN: Our Differentiated View on Estimating Losses from Downgrade and Default

To better understand the potential for credit losses from downgrades and defaults, our Applied IQ team created a proprietary tool called the Credit Health Index, or CHIN. The CHIN is a macroeconomic research tool that analyzes financial market and policy variables to give us a forward-looking view of US corporate health and a common language for discussing it. The CHIN framework then translates the corporate health view into a forecast of losses from downgrades and defaults.

For example, when a mid-cycle slowdown occurs sending markets into a tailspin, it helps us identify when prices have moved away from the fundamentals. When the CHIN is high, it indicates low potential for losses and vice versa. We can then compare the CHIN's output with spread levels to help us gauge whether we are being compensated for the risk we are taking. The result is a predictive framework that connects the Full Discretion team’s portfolio managers and strategists to the firm’s research analysts, traders and macro strategists to debate opportunities.

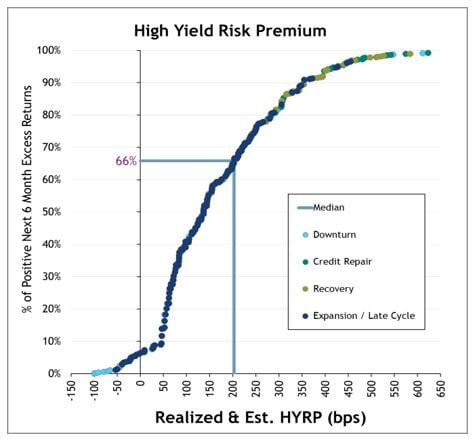

Median High Yield Risk Premium & Probability of Positive Excess Return

Source: Loomis Sayles, Bloomberg and Moody’s, as of 9/30/2025. OAS is based on the Bloomberg US Corporate High Yield Index.

The chart presented is shown for illustrative purposes only. Some, or all, of the information on these charts may be dated, and, therefore, should not be the basis to purchase or sell any securities. The information is not intended to represent any actual portfolio managed by Loomis Sayles.

This analysis is based on historical data and does not predict future results. Therefore, the use of this type of information to make investment decisions has inherent limitations. Markets may behave very differently than history suggests, it is not possible for any methodology to accurately identify and interpret all relevant market events.

Any investment that has the possibility for profits also has the possibility of losses, including the loss of principal.

Please see the Risk Premium Disclosure Statement for additional important information.

Past performance is no guarantee of future results.

Looking at current values against long-term averages also informs our understanding of whether today’s markets are cheap or rich, and then we can adjust our positioning. According to our research, as risk premiums climb, the probability of positive excess returns over the next six months also increases. We’ve found that this generally means that investors are rewarded for leaning into risk throughout the various phases of the credit cycle. However, there are times when risk premiums are on the tighter end of historical averages. We then need to allocate our risk budget accordingly, seeking opportunities in other markets or leaning into our security selection disciplines. We believe that the risk premium framework is a differentiated feature of the Full Discretion team’s investment process.

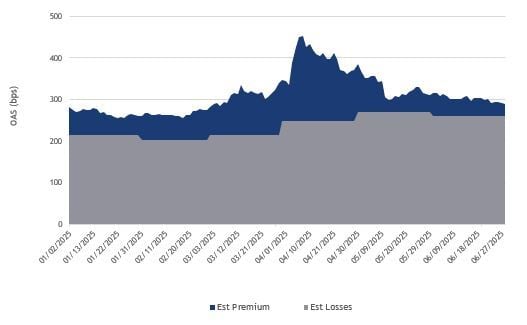

An Example of Risk Premium in Action: A Mid-Cycle Slowdown in April 2025

Source: Loomis Sayles, Bloomberg and Moody’s, as of 6/30/2025

We started 2025 in the late cycle/expansion phase, the portion of the credit cycle where the market tends to spend of the most time. As the credit markets priced in optimism toward favorable business outcomes due to anticipated Trump administration policies, risk premiums in the high yield market ground tighter. Things changed quickly over the next few months with sweeping tariffs introduced in early April. Spreads widened by over 100 basis points (bps) in a matter of days, but given the underlying strength of corporate fundamentals, we didn’t perceive an equal increase to our estimate for losses.

During this period, the risk premium approached the median for a late cycle environment, which signaled a potential buying opportunity in the high yield market. Over the course of ten days, we added a significant amount in high yield exposure across Full Discretion accounts.

In our view, the opportunity was short-lived. By the end of the month spreads had tightened again, and market data showed more signs of weakness that could indicate higher losses ahead. The risk premium framework gave the team the conviction to act quickly during challenging days.

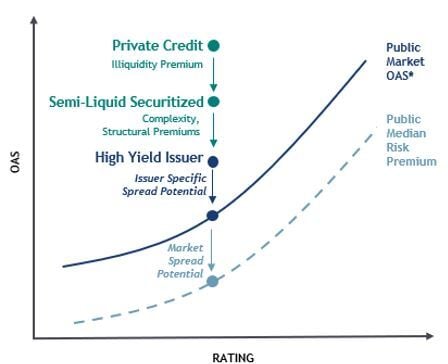

Public vs. Private Risk Premium

The Role of the Risk Premium in Public and Private Markets

When looking across our opportunity set, we tend to start with the high yield market as a base for assessing risk premium. This requires identifying and valuing key considerations to determine whether we are being adequately compensated for the risks taken. In doing so, we also focus on idiosyncratic dimensions of credit risk that may impact an issuer's performance, such as profitability and loan-to-value ratios. This investment framework provides a foundation for evaluating opportunities across the quality and liquidity spectrum, where transparency can be more limited and pricing dynamics can be less efficient, in our view.

For strategies that can invest in less liquid or private markets, there are additional factors that we’ll assess. We believe that these investments should offer additional opportunities for illiquidity, complexity and structural risks that are less common in public markets. Allocations will be made to less liquid or more complex securities when we believe we are adequately compensated for these considerations.

For decades, the Full Discretion team has invested through numerous credit cycles with both calm and turbulent markets. Our goal is to invest by measuring our risk/return through a consistent and repeatable process. The risk premium framework helps us deliver on that by leveraging a multitude of inputs to create a common understanding of credit market risk.

Making the Trade: How We Value Complex Ideas

Internet access is a both crucial and growing part of life for consumers and businesses. A national provider of fiber-based data services, and a historically large issuer in the high yield market, issued a first-time debt transaction for a fiber network securitization. The issuer offered multiple tranches with spreads ranging 350-850bps. Our deal team underwriting the investment was comprised of research analysts with diverse expertise, which helped us decompose the issue-specific traits to identify relative value.

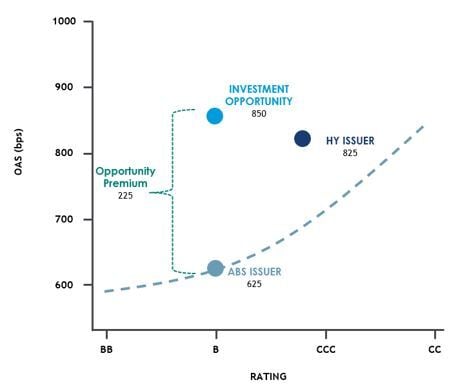

Public vs. Private Risk Premium

We evaluated the B-rated asset-backed security that was offered at 850bps using our unified research and portfolio construction process:

- At the time of syndication, B-rated asset-backed securitizations (ABS) typically traded with a spread of around 150-250bps tighter than unsecured high yield bonds of the same issuer because they often have stronger collateral security, asset backing and bankruptcy remoteness. However, that was not the case in this instance as it was offered at 850bps, which caught our attention.

- There were known risks associated with an inaugural offering and a novel approach to securitization using a retail fiber network. Given the complexity of the structure and the semi-liquid nature of the securitization, we believed that we should be offered additional spread of at least 200bps.

- Comparable unsecured high yield bonds available in the market at the time had a spread of 825bps.

- We believed that the securitization was attractive because it offered an additional 25bps of spread relative to other unsecured high yield bonds and adequately compensated for the complexity and illiquidity. Additionally, the securitization featured improved downside protection due to its collateral package and capital structure seniority.

Matt Eagan, CFA

Head of Full Discretion, Portfolio Manager

Matt Eagan, CFA

Head of Full Discretion, Portfolio Manager

Matt Eagan is a Portfolio Manager and Head of the Full Discretion Team at Loomis, Sayles & Company. He is also a member of the firm’s Board of Directors. Matt has 35 years of investment industry experience as a Portfolio Manager and Fixed Income Analyst. Matt joined Loomis Sayles in 1997 as a Fixed Income Research Analyst for the Multisector Fixed Income Team and became a Portfolio Manager in 2000. He was promoted to Co-Head of the Full Discretion Team in 2012. Previously, Matt was a senior fixed income analyst at Liberty Mutual Insurance Company and a senior credit analyst at BancBoston Financial Company. He earned a BA from Northeastern University and an MBA from Boston University.

Brian Kennedy

Portfolio Manager

Brian Kennedy

Portfolio Manager

Brian Kennedy is a Portfolio Manager on the Full Discretion Team at Loomis, Sayles & Company. He has 35 years of investment industry experience. Brian joined Loomis Sayles in 1994 as a Securitized and Government Bond Trader. He transitioned to the high yield trading desk in 2001, where he initiated the firm’s trading of bank loans, while also trading high yield, convertibles, derivatives and equities. Brian joined the Full Discretion Team as Product Manager in 2009 and was promoted to Co-Portfolio Manager of the investment grade bond product suite in 2013. In 2016, he began co-managing the entire multisector suite of products. Brian began his investment industry career as a fund accountant at the Boston Company. He earned a BS from Providence College and an MBA from Babson College.

Peter Sheehan

Portfolio Manager, Credit Strategist

Peter Sheehan

Portfolio Manager, Credit Strategist

Peter Sheehan is a Portfolio Manager on the Full Discretion Team at Loomis, Sayles & Company. He co-manages the team's suite of high yield and bank loans strategies. Additionally, Peter is a Credit Strategist focused on the bottom-up security selection process for the Full Discretion Team. Working in concert with the senior research analysts, he oversees the underwriting and investment recommendation of the team’s largest active weight positions. Peter joined Loomis Sayles in 2012 from the MBA program at Boston College. Previously, he was an associate at CapX Partners, a Chicago-based private equity firm, specializing in lower middle market and stressed credit investing. Peter began his investment industry career in the credit training program at Bank of America/LaSalle Bank. He earned a BA from Vanderbilt University and an MBA from the Carroll School of Management at Boston College.

Michael Klawitter, CFA

Portfolio Manager, Bank Loans Strategist

Michael Klawitter, CFA

Portfolio Manager, Bank Loans Strategist

Michael Klawitter is a Portfolio Manager on the Full Discretion Team at Loomis, Sayles & Company. He co-manages the team's suite of bank loans strategies. Additionally, Michael serves as a Strategist for the team, focused on bank loans. Michael began his investment career in 1997 in fund operations at First Data where he managed a group of fund specialists before joining Loomis Sayles in 2000 as a Senior Specialist in the Mutual Fund Group. After moving to the Applied Integrated Quant (Applied IQ) Team for two years, providing support to Portfolio Managers, Traders and Marketing Professionals, Michael joined the Bank Loan Team, where he analyzed credits and worked on special projects. He became a Strategist in 2013 and was promoted to Portfolio Manager in 2016. Michael earned a BA from the University at Buffalo and an MSF from Boston College. He is a CFA® charterholder.

Heather Young, CFA

Portfolio Manager, Bank Loans Strategist

Heather Young, CFA

Portfolio Manager, Bank Loans Strategist

Heather Young is a Portfolio Manager on the Full Discretion Team at Loomis, Sayles & Company. She co-manages the team's suite of bank loans strategies. Additionally, Heather serves as a Strategist for the team, focused on bank loans. Heather began her career in 2005 as a credit analyst at Columbia Management/ Bank of America, where she analyzed loans, bonds, and structured products, and developed valuation models. She joined Loomis Sayles in 2008 as a Vice President and Research Analyst covering loans, high yield, investment grade, and emerging markets credits until 2011. After earning her graduate degree, Heather then worked as an early-stage technology investor for Converge Venture Partners. Later, she was a vice president and senior analyst for ESG-forward investment grade bond manager Breckinridge Capital Advisors until 2016 when she rejoined Loomis Sayles as a Senior Bank Loan Analyst. Heather became a Strategist in 2018 and was promoted to Portfolio Manager in 2020. heather earned a BA from Boston University and an MBA from the Massachusetts Institute of Technology. She is a CFA® charterholder.

Eric Williams

Portfolio Manager

Eric Williams

Portfolio Manager

Eric Williams is a Portfolio Manager on the Full Discretion Team at Loomis, Sayles & Company. He co-manages a suite of high yield and bank loan strategies. Eric has 15 years of investment industry experience. Eric joined Loomis Sayles in 2025 from Northern Trust Asset Management where he most recently served as the head of capital structure and a senior portfolio manager on the global fixed income team. In this role, he had broad oversight of the actively-managed leveraged credit platform and served as the lead portfolio manager on several leveraged credit strategies. Previously, Eric was the head of credit at Northern Trust and a senior portfolio manager for fundamental, systematic and global high yield and ESG mandates. Prior to this, he was a portfolio manager and trader, working with research analysts to evaluate fundamental risk exposures, with a focus on valuation and volatility. Earlier in his career, Eric was a portfolio analyst and associate portfolio manager. Eric earned a BA in economics from the University of Colorado and an MBA with a concentration in finance and economics from the University of Chicago Booth School of Business.

Bryan Hazelton, CFA

Portfolio Manager, Associate Portfolio Manager, Investment Grade Strategist

Bryan Hazelton, CFA

Portfolio Manager, Associate Portfolio Manager, Investment Grade Strategist

Bryan Hazelton is a Portfolio Manager on the Full Discretion Team at Loomis, Sayles & Company. He co-manages the team’s insurance mandates and is an Associate Portfolio Manager on core plus full discretion, strategic alpha, multisector full discretion, and multisector credit mandates. Bryan also serves as a Strategist across the full discretion mandates, with a focus on investment grade credit selection. He has 18 years of investment industry experience. Bryan joined Loomis Sayles in 2011 as an Investment Analyst on the Full Discretion Team. Previously, he was a portfolio analyst at The Hartford Investment Management Company. Bryan earned a BA from Bentley University and an MBA from The Wharton School at The University of Pennsylvania. He is a CFA® charterholder and a member of the CFA Society Boston.

Chris Romanelli, CFA

Portfolio Manager, Associate Portfolio Manager, High Yield Corporate Strategist

Chris Romanelli, CFA

Portfolio Manager, Associate Portfolio Manager, High Yield Corporate Strategist

Christopher Romanelli is a Portfolio Manager on the Full Discretion Team at Loomis, Sayles & Company, where he co-manages the team’s high yield-focused insurance and buy & maintain product. He is also an Associate Portfolio Manager on the team’s suite of high yield, bank loan and multisector credit products. Additionally, Christopher is a Portfolio Strategist for the team, working closely with the team’s credit strategist on the high yield credit portion of the team’s portfolios and directly with the portfolio management team on portfolio structuring. He has 20 years of investment industry experience. Christopher joined Loomis Sayles in 2010 as a Portfolio Analyst and in 2013, he joined the Full Discretion Team as an Investment Analyst, covering high yield. Previously, he was a senior associate at PanAgora Asset Management where he provided operational support to the investment process. Christopher earned a BS from Gordon College and an MS from Boston College. He is a CFA® charterholder.

Scott Darci, CFA

Portfolio Manager, Associate Portfolio Manager, Convertibles & Equity Strategist

Scott Darci, CFA

Portfolio Manager, Associate Portfolio Manager, Convertibles & Equity Strategist

Scott Darci is a Portfolio Manager on the Full Discretion Team at Loomis, Sayles & Company. He co-manages the team’s flexible income strategies and is an Associate Portfolio Manager on the multisector full discretion and strategic alpha mandates. Scott also serves as a Strategist across the full discretion mandates, with a focus on the convertibles and equity sectors. He has 19 years of investment industry experience. Scott joined Loomis Sayles in 2008 and joined the Full Discretion Team in 2013. Prior to Loomis Sayles, he was a senior associate at Anglo Irish Bank, where he focused on interest rate and currency derivative markets. He earned a BA from Dartmouth College and a Masters in Investment Management from Boston University. Scott is a CFA® charterholder.

David Zielinski, CFA

Investment Director

David Zielinski, CFA

Investment Director

David Zielinski is an Investment Director for the Full Discretion Team at Loomis, Sayles & Company. In this role, he is responsible for articulating the team’s investment process, performance, positioning and outlook with clients, consultants and prospects. David has 28 years of investment industry experience. David joined Loomis Sayles in 2021. Previously, he was a managing director and client portfolio manager at Manulife Investment Management, where he represented the firm’s global multisector fixed income strategies. Prior to this, David was a vice president and senior product engineer for liability driven investing and fixed income index strategies at State Street Global Advisors. He earned a BS from Bryant University and an MBA from Babson College. David is a CFA® charterholder.

Cheryl Stober

Investment Director

Cheryl Stober

Investment Director

Cheryl Stober is an Investment Director at Loomis, Sayles & Company, where she covers leveraged finance, including bank loan and high yield products. She is an embedded member of both the Bank Loan and Full Discretion Teams. In this role, Cheryl is responsible for articulating each team’s investment process, performance, positioning and outlook with clients, consultants and prospects. Cheryl joined Loomis Sayles in 2005 as a Senior Operations Analyst. In 2007, she joined the Bank Loan Team as a Portfolio Assistant and became the team’s Investment Director in 2013. She expanded her role in 2023 by joining the Full Discretion Team. Previously, Cheryl worked in bank loan operations at Bain Capital. Cheryl earned a BA in economics from Brandeis University and an MBA from Boston University.

Kristen Doyle

Associate Investment Director

Kristen Doyle

Associate Investment Director

Kristen Doyle is an Associate Investment Director for the Full Discretion Team at Loomis, Sayles & Company. In this role, she is responsible for supporting the growth and retention of full discretion assets. Kristen has 18 years of investment industry experience. Kristen joined Loomis Sayles in 2012 as a Portfolio Analyst where she completed client and ad hoc reporting, prepared meeting materials and provided support to the relationship managers. She joined the Full Discretion Team as an Investment Analyst in 2014. Previously, Kristen was a registered client associate at Mayflower Advisors. She earned a BS from the Carroll School of Management at Boston College and an MBA from Boston University.