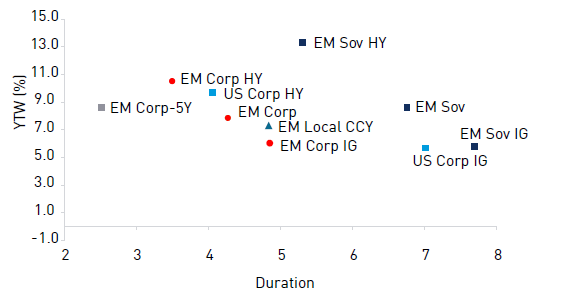

FIGURE 1 - YIELD VERSUS DURATION

as of 30 September 2022

Sources: Loomis Sayles, J.P. Morgan, Barclays, Merrill Lynch, and Bloomberg LP. Data as of 30 September 2022. See Endnotes for indices used. Indices are unmanaged and do not incur fees. It is not possible to invest directly in an index. This marketing communication is provided for informational purposes only and does not represent the actual or expected future performance of any investment product

Past market experience is no guarantee of future results.

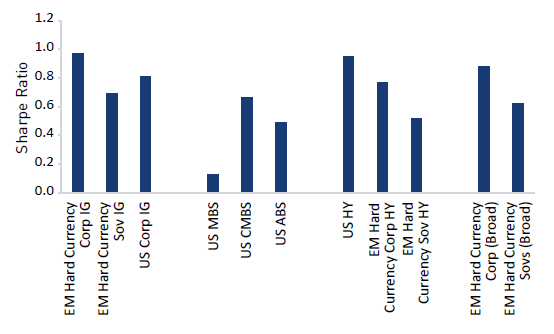

FIGURE 2 - RISK-ADJUSTED RETURNS

Sources: J.P. Morgan, ICE BofA. Based on weekly returns annualized 31 December 2011 to 31 December 2021. See Endnotes for index names.

Past market experience is no guarantee of future results.

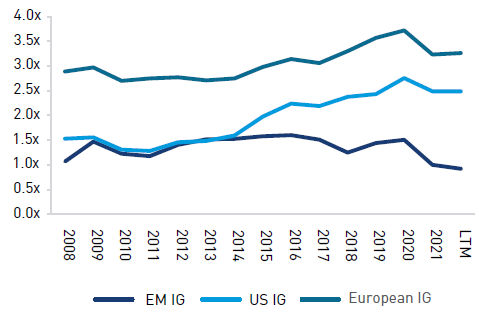

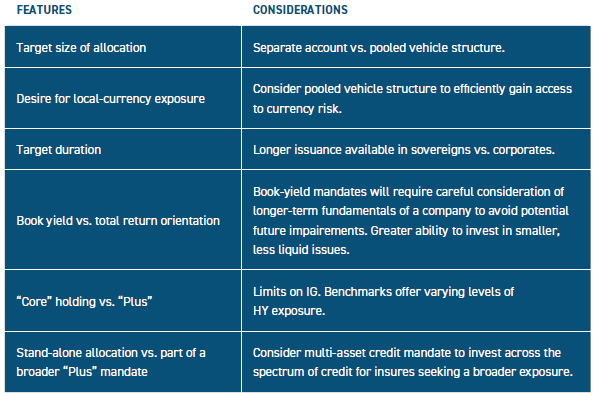

NET LEVERAGE COMPARISON

EM IG VS. DM IG

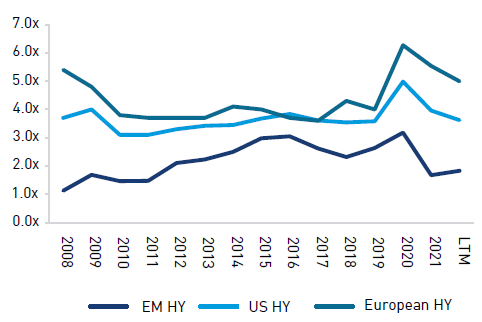

Sources for right and left chart: J.P. Morgan, Bloomberg, CapitalIQ.

As of September 2022 (most recent data available).

NET LEVERAGE COMPARISON

EM HY VS. DM HY

SPREAD COMPARISON 5-YR BB

Sources for right and left chart: Loomis Sayles, as of 30 September 2022. Indices are unmanaged and do not incur fees. It is not possible to invest directly into an index. Indices do not represent the actual or expected future performance of any investment product.

Past market experience is no guarantee of future results.

SPREAD COMPARISON 5-YR BBB

Endnotes

Yield versus Duration chart:

EM Sov HY = J.P. Morgan Emerging Markets Bond Index, EM Corp HY = J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI) Broad Diversified High Yield, EM CORP IG = J.P. Morgan CEMBI Broad Diversified Investment Grade Index, EM Sov IG= J.P. Morgan EMBI Global Investment Grade Index, US HY = Bloomberg Barclays US High Yield Index, US IG = Bloomberg Barclays US Aggregate Corporates, EM Corp = J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI Broad Diversified), EM CORP 1-5yr = 50% J.P. Morgan CEMBI Broad Diversified 1-3year Index, 50% J.P. Morgan CEMBI Broad Diversified 3-5year Index.

Sharpe Ratio Chart:

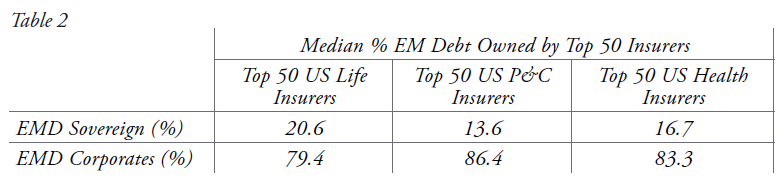

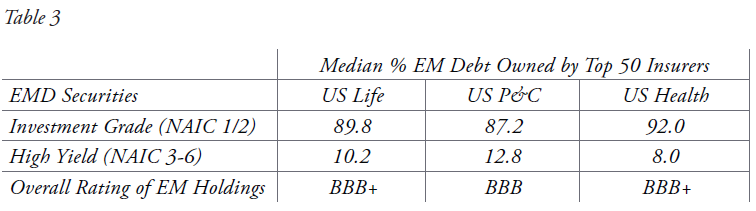

Source: S&P Global Market Intelligence / Bloomberg. As of 31 December 2021. Top 50 based on YE 2020 Total Assets.

Source: S&P Global Market Intelligence / Bloomberg, As of 31 December 2021. Top 50 based on YE 2021 Total Assets.

Source: S&P Global Market Intelligence / Bloomberg. As of 31 December 2021. Top 50 based on YE 2021 Total Assets.

NAIC: National Association of Insurance Commissioners.

Disclosure

This marketing communication is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only, and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted or that actual results will be different. Data and analysis does not represent the actual, or expected future performance of any investment product. Information, including that obtained from outside sources, is believed to be correct, but Loomis cannot guarantee its accuracy. This information is subject to change at any time

without notice.

Diversification does not ensure a profit or guarantee against a loss.

Any investment that has the possibility for profits also has the possibility of losses, including loss of principal.

Indexes are unmanaged and do not incur fees. It is not possible to invest directly in an index.

Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization.

LS Loomis | Sayles is a trademark of Loomis, Sayles & Company, L.P. registered in the US Patent and Trademark Office.

MALR030322