ECOSYSTEM SERVICES

Source: Loomis Sayles.

VALUATION

Leading academic research on ecosystem services in 2011 (most recent data available) put its total annual value at $124.8 trillion.2,3 This figure is an estimate for the value of all ecosystem services, many of which are hard to put a monetary value on like air quality, soil formation and pollination. Additionally, natural assets play a critical role in the global economy. According to the World Economic Forum (2020), more than fifty percent of the world’s GDP is moderately or highly dependent on nature and its services. Nature’s contribution to the global economy is estimated to be $44 trillion of economic value generated per year.4 To put these two values in context, global GDP in 2022 was $101 trillion.

While a complete collapse might be unlikely, especially over a short- to medium-term horizon, any decline of biodiversity presents rising physical and transition risks to the financial system. Additionally, over time we may see a higher correlation between biodiversity and financial performance driven by technical factors. This could include increased market scrutiny and significant focus on the financial materiality of biodiversity factors.

IMPORTANCE OF LOCATION

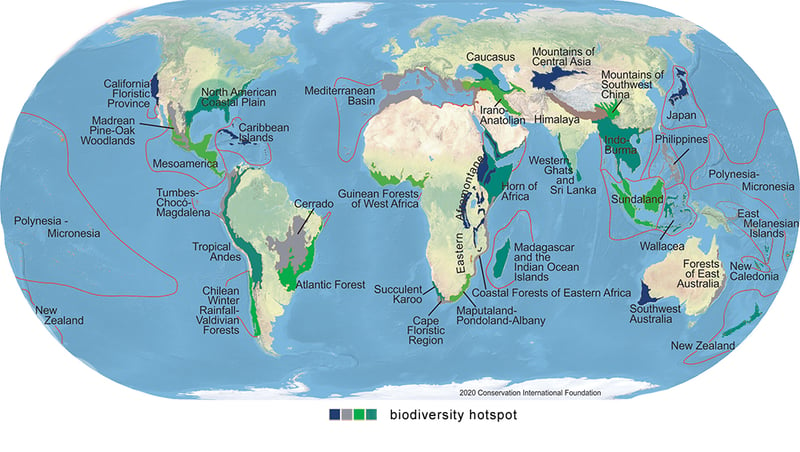

Biodiversity is not evenly distributed globally. There are currently 36 hotspots, which now represent just 2.3% of the world’s land area. These hotspots initially covered 15.9% of Earth but habitat destruction has led to this depletion.5

Many biodiversity hotspots are located in emerging markets (EM), elevating potential risks in these countries. Additionally, EM economies tend to be more reliant on ecosystem services, such as agriculture, forestry, fisheries and commodities.

GLOBAL BIOLOGICAL HOTSPOTS

Source: 2020 Conservation International Foundation. Legend colors distinguish adjacent hotspots.

Source: 2020 Conservation International Foundation. Legend colors distinguish adjacent hotspots.

SOVEREIGN SENSITIVITY

Currently, credit rating agencies do not explicitly take biodiversity and nature-related risks into account. But these risks could have significant impacts on sovereign creditworthiness, default probability and the cost of capital, which also has implications for companies in those countries.6

In general, analysts project global deterioration of ecosystem services over time. This implies negative rating trajectories that corporations and countries would be wise to consider.

If a country were to face a partial ecosystem collapse, its debt spreads would likely widen—especially for those facing significant default risk and higher funding costs. In turn, corporations doing business there would face higher borrowing costs and wider spreads on the back of country pressures. Additionally, we believe there would be potential for broad global economic and sentiment implications that could drive a repricing across regions.

While developed markets (DM) may have fewer physical risk concerns, they have significant ecological footprints due to their trade with emerging countries. The strain that DM trade can place on resources in emerging countries that may have more fragile biodiversity has prompted calls similar to the “fair share” discussion in climate change.7

CORPORATE VULNERABILITIES

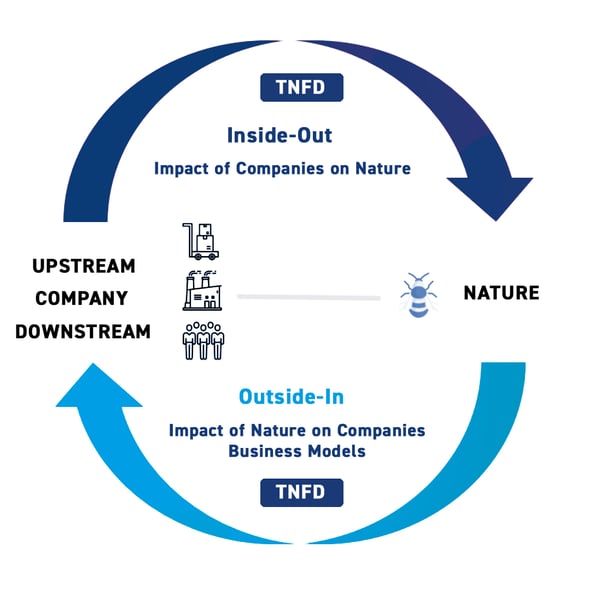

Unlike carbon emissions, where only the impact from companies is measured, biodiversity encompasses a concept called double materiality—an entity’s impact on natural resources and its dependency on natural resources.

Double materiality is a relatively new concept in financial reporting. To date, the Financial Stability Board’s Task Force on Climate-related Financial Disclosures (TCFD) has recommended entities report only their dependencies.8 We expect double materiality will be a key aspect of the Task Force on Nature-related Financial Disclosures (TNFD)’s final framework, expected in September 2023.

Source: https://kpmg.com/nl/en/home/insights/2021/11/its-time-to-act-on-nature-related-risk.html

Source: https://kpmg.com/nl/en/home/insights/2021/11/its-time-to-act-on-nature-related-risk.html