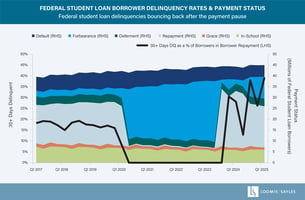

Graphic Source: Loomis Sayles. Views as of 11 June 2025. The graphic presented is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and, therefore, should not be the basis to purchase or sell any securities. Any opinions or forecasts contained herein reflect the current subjective judgments and assumptions of the authors only, and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. This information is subject to change at any time without notice.

Table Source: Loomis Sayles. Views as of 11 June 2025. Highlighted cells represent attributes we’re currently observing. Green represents our current view. Bright blue represents the previous view (if different from the current view). Arrows indicate the direction of change in view where applicable. The table presented is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and therefore, should not be the basis to purchase or sell any securities.